Which one of the following statements about Unified Payments Interface (UPI) and Central Bank Digital Currency (Digital Rupee) is not correct ?

- AUPI is a real-time payment system but Digital Rupee is akin to sovereign paper currency.

- BIn case of UPI, settlement for end users happens instantly as the money gets immediately debited or credited but in case of Digital Rupee, there is no settlement as the wallet balance gets transferred to another wallet.

- CUPI transactions are recorded by banks and reflected in bank statements but in case of Digital Rupee, no data is captured in bank statements as transactions are from one wallet to another.

- DIn both the cases (UPI and Digital Rupee), the liability lies with the users and their respective banks.Correct

Explanation

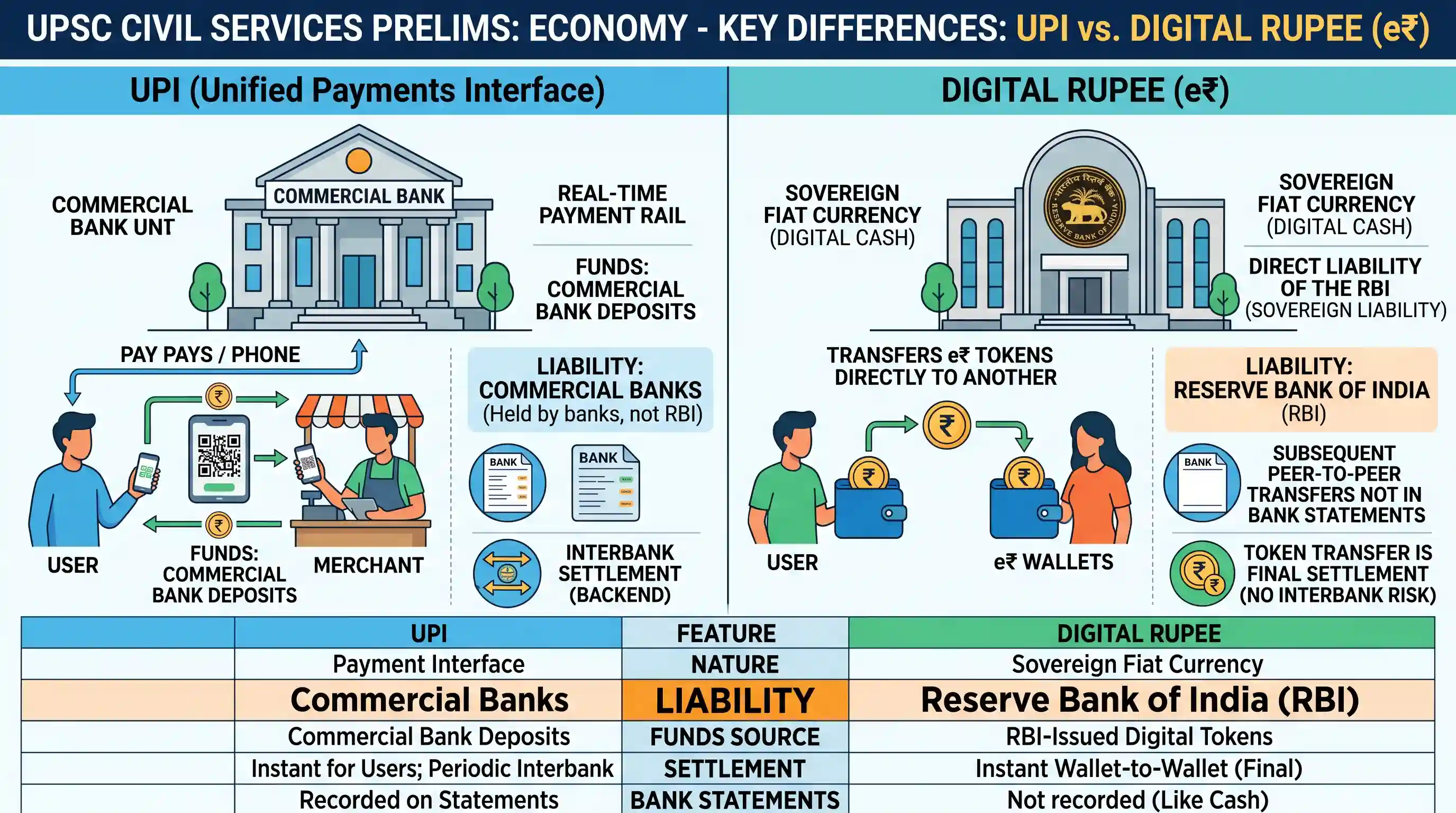

Option D is the incorrect statement, making it the correct answer. The critical distinction between the Unified Payments Interface (UPI) and the Digital Rupee lies in the nature of the liability. According to the Reserve Bank of India (RBI), which launched the retail Central Bank Digital Currency (CBDC) pilot on December 1, 2022 [4], the Digital Rupee (e₹) is a sovereign fiat currency. Under Section 26 of the RBI Act, 1934, it represents a direct liability of the central bank (the RBI) [3]. In contrast, funds transferred via UPI are commercial bank deposits, meaning the liability lies with the respective commercial banks [4].

Here is why the other options are correct statements and thus not the answer:

- Option A: This is correct. UPI is a real-time payment interface (a transfer infrastructure developed by NPCI), whereas the Digital Rupee is actual sovereign digital cash [3, 8].

- Option B: This is correct. With UPI, user accounts are debited/credited instantly, but backend interbank settlement occurs periodically. For the Digital Rupee, the wallet-to-wallet token transfer itself constitutes the final settlement, completely eliminating interbank settlement risk—just like handing over physical paper notes [2, 3].

- Option C: This is correct. Every UPI transaction is routed through core banking systems and recorded on commercial bank statements. Digital Rupee transactions are executed directly between e₹ wallets; once funds are withdrawn into the wallet, subsequent peer-to-peer transfers do not reflect on standard bank statements, offering cash-like privacy [7].

Takeaway: UPI is the rail that moves your money (commercial bank liability), whereas the Digital Rupee is the money itself (direct RBI liability).

Related questions

More UPSC Prelims practice from the same subject and topic.

- Prelims 2026GS1economy

Which one of the following correctly represents the three key sub-indices of the Financial Inclusion Index (FI-Index) of the Reserve Bank of India (RBI) ?

- Prelims 2026GS1economy

Which of the following statements about M1xchange's role in Micro, Small & Medium Enterprises (MSMEs) financing is/are correct ? 1. M1xchange provides collateral based loans to MSMEs. 2. M1xchange fac…

- Prelims 2026GS1economy

Consider the following statements with reference to the Sagarmala Programme of the Government of India : I. The Sagarmala Programme seeks to achieve port-led economic growth through cost-effective and…

- Prelims 2026GS1economy

In what way(s) does the Vizhinjam International Seaport represent a structural shift in India's maritime trade and logistics policy? 1. By functioning exclusively as a domestic cargo hub to reduce rel…

- Prelims 2026GS1economy

An e-commerce revenue model where the seller has control over pricing but doesn't keep products in stock and instead transfers customer orders and shipment details to a third-party supplier, who then …

- Prelims 2026GS1economy

Which one of the following best describes the key objective of India's 'Open Network for Digital Commerce' (ONDC) initiative ?