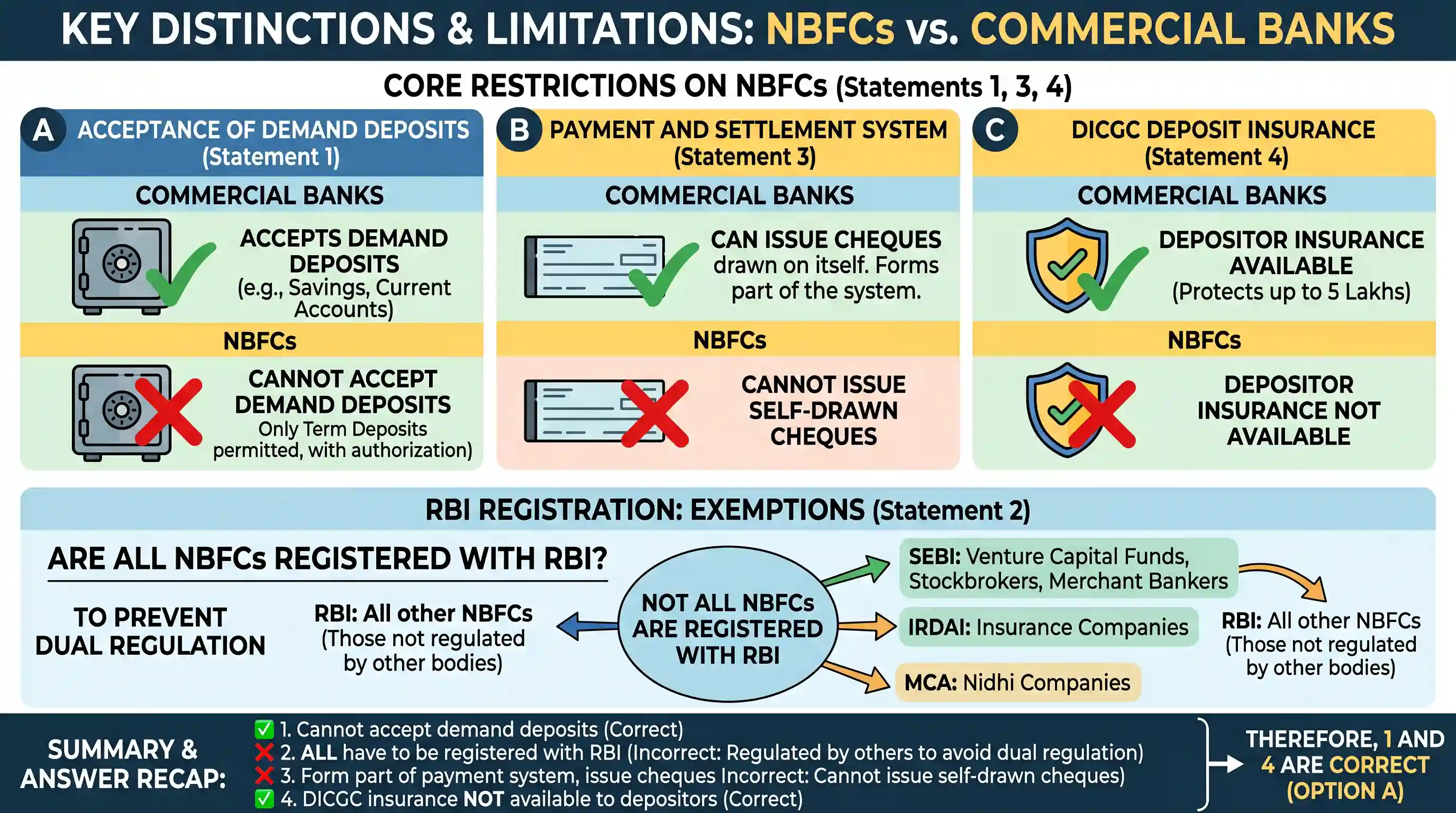

Consider the following statements about the Non-Banking Financial Companies (NBFCs) in India : 1. NBFCs cannot accept demand deposits. 2. All the NBFCs operating in India have to be registered with the RBI. 3. NBFCs form part of the payment and settlement system and can issue cheque drawn on itself. 4. Deposit insurance facility of Deposit Insurance and Credit Guarantee Corporation (DICGC) is not available to the depositors of deposit taking NBFCs. Which of the statements given above is/are correct ?

- A1 and 4Correct

- B1, 2 and 3

- C4 only

- D2, 3 and 4

Explanation

Correct Answer: Option A (1 and 4)

Statement 1 is correct: Non-Banking Financial Companies (NBFCs) are strictly prohibited from accepting demand deposits (such as savings or current accounts). They are only permitted to accept term (fixed) deposits, provided they hold a specific deposit-taking Certificate of Registration from the Reserve Bank of India (RBI).

Statement 2 is incorrect: It is a misconception that all NBFCs must register with the RBI. To prevent dual regulation, the RBI explicitly exempts NBFCs that are regulated by other statutory bodies from its registration requirements. For example, venture capital funds, stockbroking companies, and merchant banking companies register with the Securities and Exchange Board of India (SEBI); insurance companies are regulated by the Insurance Regulatory and Development Authority of India (IRDAI); and Nidhi companies fall under the Ministry of Corporate Affairs.

Statement 3 is incorrect: Unlike commercial banks, NBFCs do not form part of the national payment and settlement system. Consequently, they lack the legal authority to provide cheque-based transaction facilities or issue cheques drawn on themselves.

Statement 4 is correct: The deposit insurance facility offered by the Deposit Insurance and Credit Guarantee Corporation (DICGC)—which protects commercial bank depositors—is exclusively available to banks. It does not cover the depositors of deposit-taking NBFCs, meaning funds placed with them carry a different risk profile.

Key Takeaway: While NBFCs perform bank-like functions in lending and investing, they differ fundamentally from banks. Remember the three major "Cannots" of an NBFC: They cannot accept demand deposits, cannot issue self-drawn cheques, and cannot offer DICGC deposit insurance.

Related questions

More UPSC Prelims practice from the same subject and topic.

- Prelims 2026GS1economy

Consider the following statements with reference to the Sagarmala Programme of the Government of India : I. The Sagarmala Programme seeks to achieve port-led economic growth through cost-effective and…

- Prelims 2026GS1economy

In what way(s) does the Vizhinjam International Seaport represent a structural shift in India's maritime trade and logistics policy? 1. By functioning exclusively as a domestic cargo hub to reduce rel…

- Prelims 2026GS1economy

An e-commerce revenue model where the seller has control over pricing but doesn't keep products in stock and instead transfers customer orders and shipment details to a third-party supplier, who then …

- Prelims 2026GS1economy

Which one of the following correctly represents the three key sub-indices of the Financial Inclusion Index (FI-Index) of the Reserve Bank of India (RBI) ?

- Prelims 2026GS1economy

Which one of the following best describes the key objective of India's 'Open Network for Digital Commerce' (ONDC) initiative ?

- Prelims 2026GS1economy

Which one of the following statements about Unified Payments Interface (UPI) and Central Bank Digital Currency (Digital Rupee) is not correct ?